Tax Software

The client calls at 4 PM on a Thursday.

They got an IRS notice. They owe more than they can pay. Collection action might already be on the table. They are scared, confused, and very much expecting you to fix it.

You know exactly what the next step is: a monthly installment agreement. You have done it a hundred times. But here is what most firms do not talk about — the actual workflow behind Form 9465 is only as clean as the system holding it together.

The form is four pages. The process around it? That is the whole job.

This is a guide for tax resolution teams who want to stop treating Form 9465 as a one-off task and start building it into a repeatable, documented case setup workflow that holds up at volume.

Form 9465 is the IRS Installment Agreement Request. It is the formal mechanism by which a taxpayer requests a monthly payment plan for an outstanding balance they cannot pay in full today.

The IRS's own instructions for Form 9465 break this down clearly. For balances of $50,000 or less, taxpayers may not even need to file the paper form. They can apply through the IRS Online Payment Agreement (OPA) tool, which carries a lower setup fee. For balances above $50,000, Form 9465 is required, and it almost always needs to be accompanied by Form 433-F, the Collection Information Statement, so the IRS can verify the taxpayer's financial situation.

As of July 1, 2024, setup fees are:

Low-income taxpayers, those at or below 250% of the federal poverty guidelines, may qualify for reduced or waived fees.

And critically: approval does not stop the clock. Interest and late-payment penalties continue to accrue on the unpaid balance until it is paid in full. Your client needs to understand that going in.

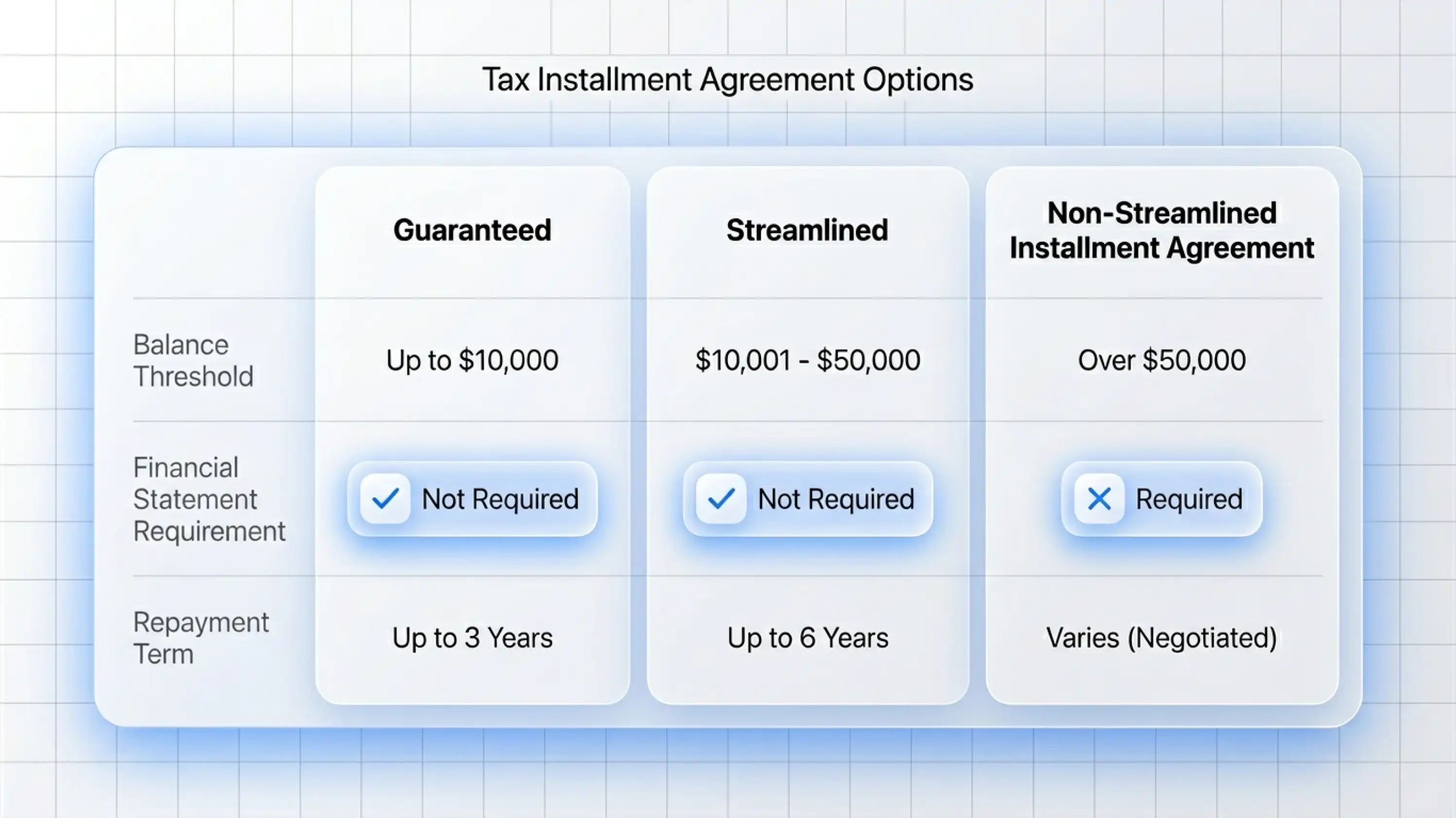

Not every Form 9465 case lands in the same bucket. One of the first assessments your team has to make is which type of agreement applies, because that shapes everything from the documentation requirements to the timeline.

Guaranteed Installment Agreement

Available when the balance owed is $10,000 or less, all required returns are filed, and the client has not entered into an installment agreement in the previous five years. Approval here is nearly automatic if the client agrees to pay within three years.

Streamlined Installment Agreement

The most common path for tax resolution firms. Available for balances up to $50,000. No financial statement required. Full repayment within 72 months or before the Collection Statute Expiration Date, whichever comes first. This is typically the first option to explore for clients who do not qualify for an OIC.

Using the IRS Online Payment Agreement tool here keeps fees lower and often gets faster confirmation than the paper form route.

Non-Streamlined Installment Agreement

For balances above $50,000, the work gets real. Form 9465 plus Form 433-F, a full financial disclosure. The IRS reviews the client's income, expenses, and assets before agreeing to terms. This is not a form submission. This is a negotiation.

Knowing which category the client falls into before anyone touches Form 9465 is how resolution teams stop wasting time on the wrong path.

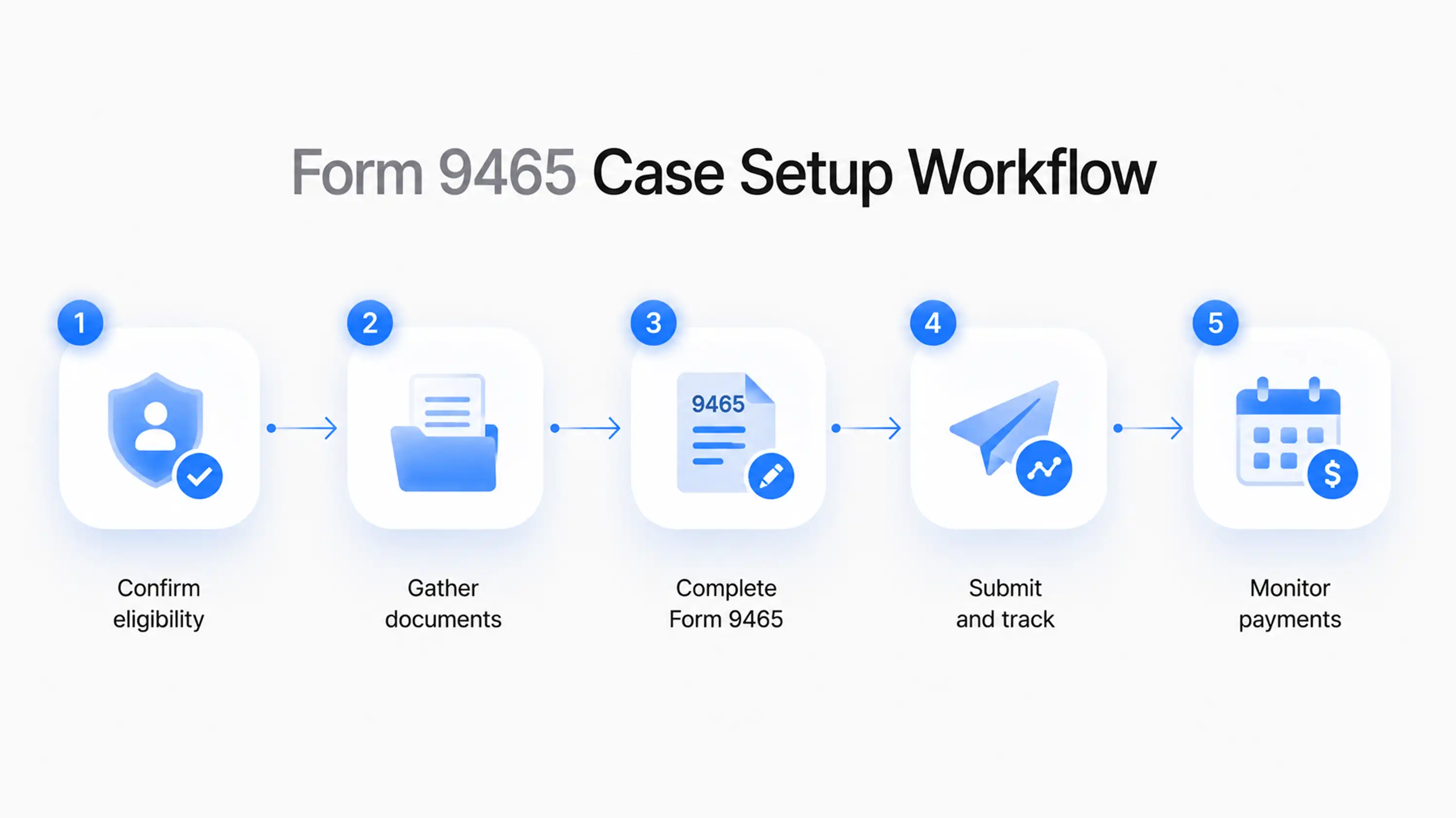

This is where most firms have room to improve. The form is not the bottleneck. The case setup around it is.

Here is what a clean workflow looks like from intake to submission:

Step 1: Confirm eligibility and agreement type

Before any form is touched, pull the client's current balance and confirm all required returns are filed. Missing filings block approval. One unfiled year is enough to sink an otherwise clean streamlined agreement request.

Firms that run financial questionnaires through their case management platform can automate much of the intake process. The client fills in their financial picture once. The data flows directly into the relevant IRS forms without manual re-entry.

Step 2: Gather and organize client documents

For guaranteed and streamlined agreements, documentation is minimal. For non-streamlined cases, you need Form 433-F at minimum, which means bank statements, pay stubs, utility bills, and a full accounting of assets and monthly expenses. This document-collection step is where cases most often stall.

A structured document collection workflow with clear status tracking makes the difference between a case that moves and one that sits in an inbox for three weeks waiting on a bank statement.

Step 3: Complete and review Form 9465

Key fields to get right:

If the balance exceeds $50,000, attach Form 433-F. Submitting without it is one of the most common reasons for denial.

Step 4: Submit and track

Paper Form 9465 is mailed to the IRS Service Center for the client's state. If filing alongside a return, it goes on top of the return package. If filing standalone, the July 2024 instructions include a full table of addresses by state.

Online submissions through OPA give faster confirmation and lower fees. For most streamlined agreement cases, this is the better path.

Step 5: Document everything and set payment reminders

Once the agreement is approved, the case does not close. The client needs to make payments consistently. One missed payment can terminate the agreement. Your team needs a billing system that tracks installment payment history, flags missed payments, and ties each payment to the correct invoice in the case record.

Resolution teams see the same errors on repeat. Here are the ones worth building checkpoints around:

Proposing an unrealistic monthly payment. The IRS will often accept what the client proposes. If the client cannot actually sustain that amount, default comes quickly and getting a second agreement approved is significantly harder.

Submitting with missing or unfiled returns. The IRS will not approve an installment agreement while returns are outstanding. Confirm filing status before submission, not after.

Ignoring interest and penalty accrual. Approval stops most collection action. It does not stop interest. Clients need a clear picture of the total cost before they decide whether an installment agreement is the right path or paying in full with a loan.

Missing the 433-F for balances over $50,000. The form is incomplete without it. This is a predictable, preventable denial.

Losing track of the agreement after approval. The case does not end when the IRS approves the plan. Payment tracking, annual IRS account reviews, and watching for new notices are all ongoing.

Tax resolution teams filing Form 9465 cases at volume need more than a form library. They need a platform that supports the full workflow from intake to approval to payment tracking, without spreadsheets, separate billing tools, or manual data re-entry.

IRSLogics is built for exactly this kind of case lifecycle. The Financial Questionnaire sends a fillable financial intake form directly to the client. When they complete it, the data auto-populates into IRS financial forms inside the platform, including the information needed for Form 433-F. The Document Collection workflow tracks every file with status visibility, so case managers always know what has been received and what is still outstanding.

On the billing side, the Tying Payments to Invoices feature connects every client payment to its specific invoice. For installment agreement cases where clients are making monthly payments over months or years, this is not optional. It is how your accounts receivable stays accurate without a reconciliation exercise at the end of every billing cycle.

The Client Portal provides clients with a secure place to view their case status, make payments, upload documents, and communicate with the firm, without email threads falling through the cracks. For resolution cases that run six to eighteen months, that communication infrastructure matters.

See how IRS Logics handles installment agreement cases from intake to close.

For tax debts of $50,000 or less with all returns filed, the IRS Online Payment Agreement (OPA) is usually the best option because it is faster and provides immediate confirmation. Form 9465 is typically used for balances over $50,000, paper submissions, or situations where online filing is not possible.

Yes, if the tax debt exceeds $50,000. The IRS uses Form 433-F to evaluate the client's financial ability to pay. For streamlined agreements of $50,000 or less, Form 433-F is not required.

Online applications can be approved almost immediately for qualifying cases. Paper applications take longer and may require additional documentation.

Missing a payment can put the agreement into default and restart IRS collection actions. While reinstatement is possible, it is not guaranteed, which is why ongoing payment monitoring is critical.

Yes. For streamlined agreements, payments must satisfy the balance within 72 months. For larger balances, the IRS reviews the client's financial information and may adjust the proposed payment amount.

No. An installment agreement can stop most collection actions, but interest and penalties continue to accrue until the balance is paid in full.

Form 9465 is a four-page form. The workflow around it is a case management problem.

For tax resolution teams handling these cases at any real volume, the difference between a smooth process and a constant scramble comes down to the system behind the form. Clean intake, structured document collection, realistic payment proposals, and billing that tracks every installment against the right invoice.

Build the workflow right, and Form 9465 cases become one of the most repeatable, manageable parts of a resolution practice. Do it without infrastructure, and every case starts from scratch.

All

Tax Software

Workflow & Automation

Industry News

Resolution Tips

Tax Resolution Marketing

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Share this article directly by email. Simply enter the recipient’s details below.

Article has been send to you.