Tax Software

Most tax resolution deals do not fall apart because the client does not need help. They fall apart because the client cannot afford the next step.

A client may be ready to resolve their IRS debt, but if the payment conversation is vague or the options are unrealistic, the case slows down, the client hesitates, and your team ends up chasing paperwork and payments.

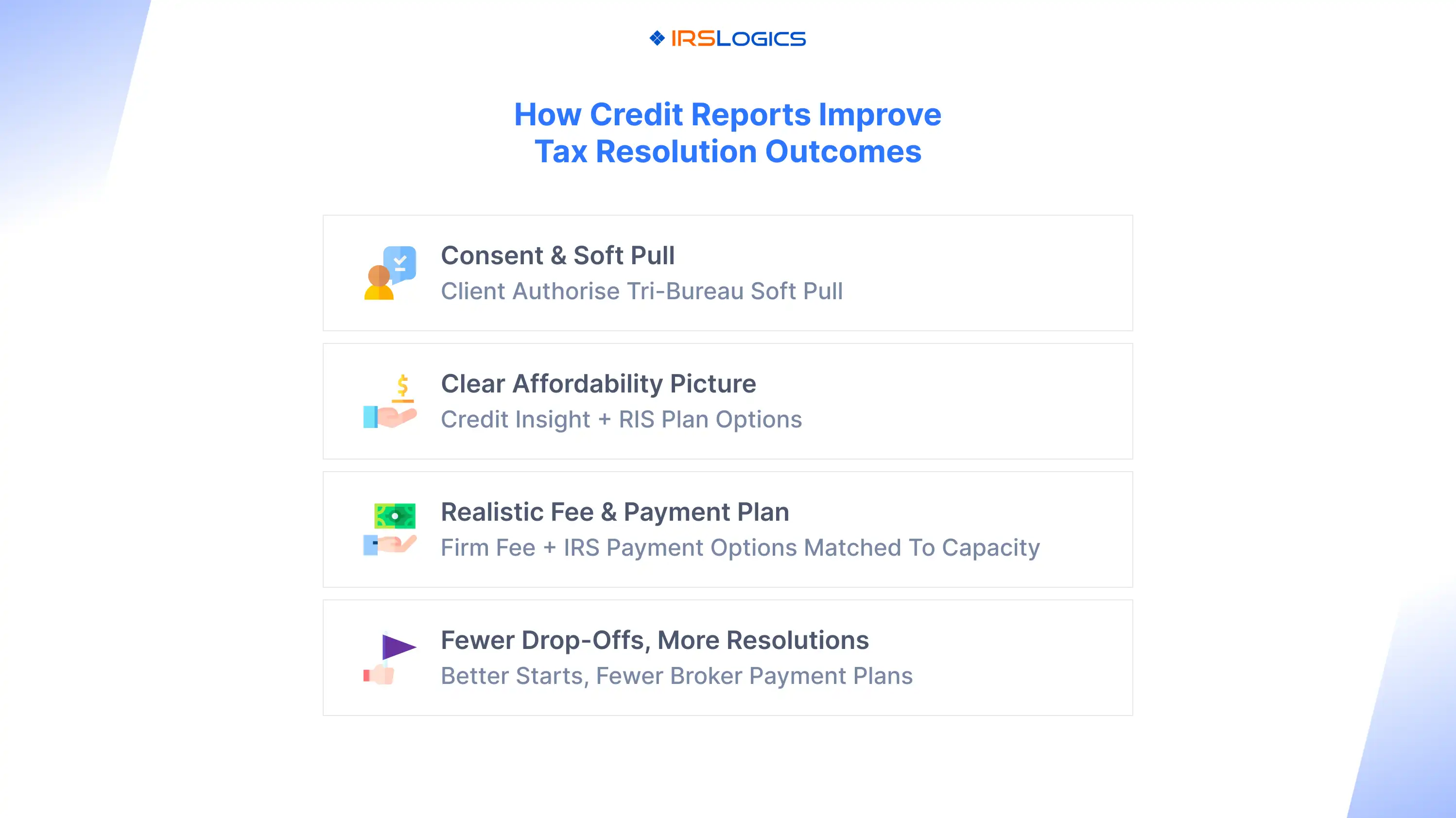

Credit insights, used the right way and with the right permissions, help you close that affordability gap with clarity. They let you pre-qualify, set expectations early, and connect clients to realistic payment paths, without turning your firm into a bank.

From an owner’s perspective, the strongest marketing and sales process can still lose momentum at one moment, the moment the client asks, how am I going to pay for this?

That question shows up in two places:

The IRS itself acknowledges that taxpayers may explore different ways to pay, including loans, and notes that, in some situations, a loan may cost less than ongoing IRS interest and penalties.

It also explains installment agreements as a formal way to pay over time.

When you cannot guide a client to a realistic payment plan, you get more cancellations, more broken payment arrangements, and more cases that never reach resolution.

Credit reports are not about curiosity. In a tax resolution firm, they support three outcomes that directly affect revenue and case throughput.

Clients often self-report their credit as “good” or “terrible,” and both are frequently wrong. A credit report gives you an objective starting point for an honest affordability discussion.

If the client is likely to qualify for financing, you can present options confidently. If they are unlikely, you can avoid wasting weeks building a plan around funding that will not happen.

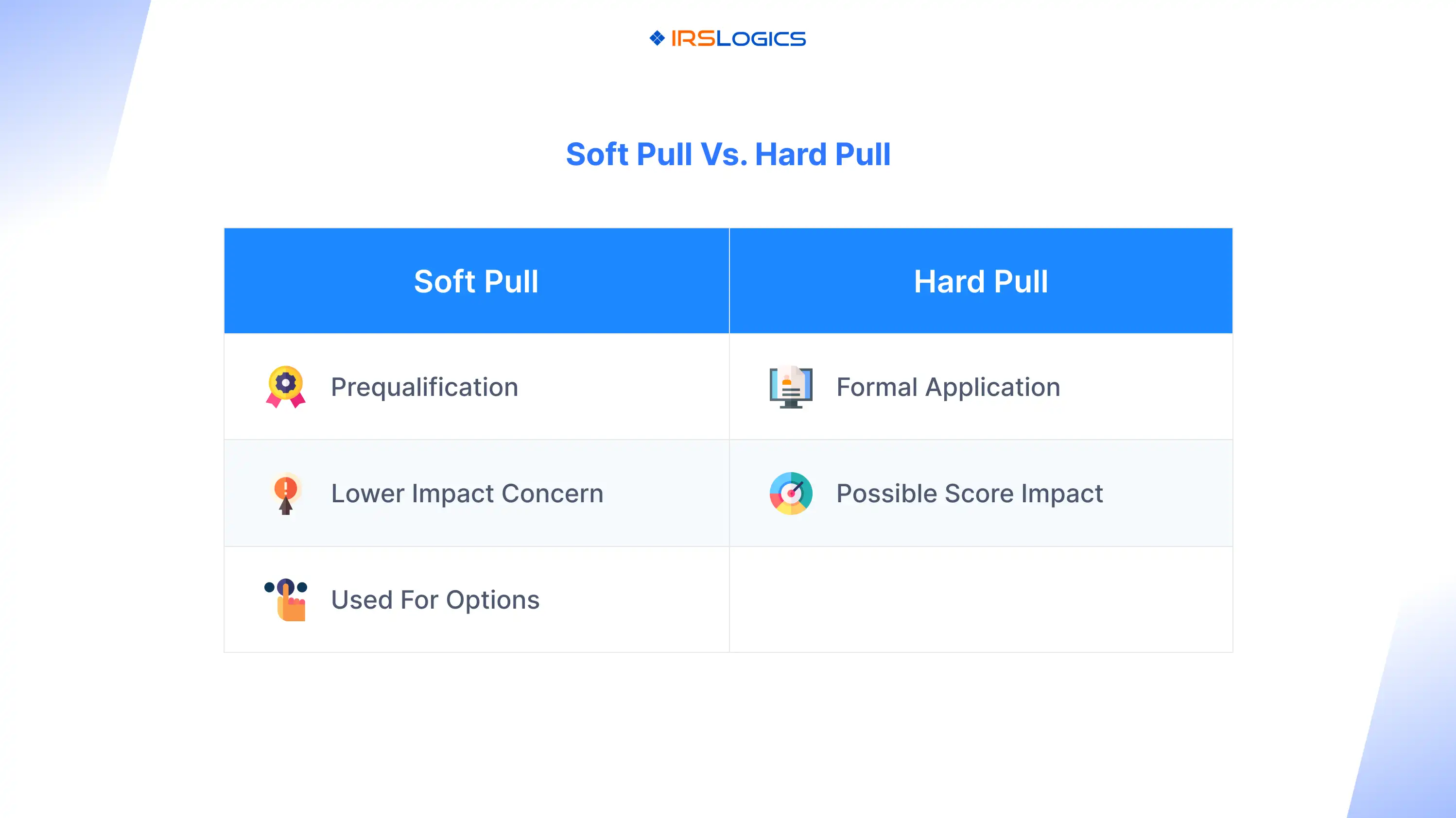

Credit reporting providers position soft-pull tools specifically for prequalification, so businesses can match customers to appropriate terms earlier in the process.

When a client understands what is realistic, they are less likely to disappear when it is time to pay for onboarding, documentation, or a resolution package.

Prequalification is often described as a low-risk way to gauge eligibility and potential terms before a formal application, typically using a soft inquiry.

Your goal is not to promise financing. Your goal is to replace uncertainty with clear next steps.

Better financing conversations lead to better outcomes:

That is the operational reason credit belongs in tax resolution.

When firms decide to use credit data, the next question is whether they are looking at a partial picture or the full picture.

Tri-bureau access matters because it reduces surprises. A client may look different across bureaus, and financing decisions often rely on more than one bureau or a merged view.

iSoftPull specifically positions access to all three major bureaus through a single agreement and single integration, which supports the “tri-bureau in one place” narrative.

It also describes tri-merge reporting as a combination of individual reports from the three national credit bureaus.

For owners and sales leaders, the takeaway is simple. More complete credit visibility improves the quality of the payment conversation, which reduces the odds that a case stalls after onboarding.

You do not need to over-explain credit pulls to clients, but you do need to explain them clearly.

A soft pull is typically used for prequalification and does not have the same impact on scores as a hard pull.

Credit platforms also commonly distinguish between soft pulls for prequalification and hard pulls when a consumer is applying for a loan, and they emphasize the need for permission.

A client-friendly script that keeps things simple:

We can run a consent-based credit check to help us understand which payment options are realistic. It helps us avoid guessing and saves time. This does not obligate you to apply for anything.

This is the part many articles skip, and it is the part you should treat as non-negotiable.

The Fair Credit Reporting Act limits when consumer report information can be provided and requires that it be for a permissible purpose.

The CFPB has also published guidance emphasizing that permissible purposes are consumer-specific and must be handled carefully.

Practical guardrails for a tax resolution firm:

Here is how owners and sales leaders typically apply credit insights without turning the firm into a lender.

When your team understands likely affordability early, you can recommend a fee structure the client can actually sustain, rather than one that looks good on paper but collapses in month two.

That reduces refunds, chargebacks, and stalled cases.

Clients commonly ask whether they should borrow to pay the IRS. The IRS itself notes that taxpayers may consider a loan in some cases, and that it may cost less than ongoing interest and penalties.

At the same time, an IRS payment plan may be the right answer for many clients.

Credit insights help you handle that conversation responsibly:

Drop-off often occurs when clients leave the call unsure. Credit-informed prequalification reduces uncertainty. It also helps your team avoid sending clients on a scavenger hunt for “proof of credit” or asking them to pull their own report and email it back.

Credit platforms position integrated credit access as a way to view reports within your own system, reducing friction and keeping the client experience consistent.

This strategy works best when it lives inside your core system, not in scattered tools and inboxes.

IRSLogics positions itself as a tax resolution CRM that unifies case management, client collaboration, forms, reporting, and integrations, which is the operational foundation you need for a clean financing and payment workflow.

The practical goal is continuity:

If you want to frame this feature on your site or in sales enablement, the message is not “we pull credit.” The message is “we help clients understand realistic payment paths early, so cases move forward.”

They do not replace IRS financial analysis, but they can help you understand a client’s broader credit picture and likely financing options, which can affect how you structure fees and timelines.

Soft inquiries are generally used for prequalification and are considered a risk-free way to gauge eligibility without the same score-impact concerns as hard inquiries.

Credit reporting providers commonly emphasize that permission is required, and federal rules restrict access to consumer reports without a permissible purpose. Treat consent as mandatory in your process and confirm requirements for your specific use case.

Tri-bureau access reduces the chance of surprises and gives a more complete view for prequalification and financing conversations. iSoftPull positions tri-bureau access through a single integration and also explains tri-merge reporting.

The IRS says taxpayers have multiple payment options and notes that a loan may be worth considering in some cases, because it could cost less than ongoing interest and penalties.

Credit reports belong in tax resolution because they solve a real business problem, the affordability gap between a client’s intent to resolve and their ability to pay. Tri-bureau insights help you pre-qualify, set expectations early, and guide clients toward realistic payment paths, including IRS payment plans and other funding options, while reducing drop-off and improving payment outcomes.

Key Takeaway

All

Tax Software

Workflow & Automation

Industry News

Resolution Tips

Tax Resolution Marketing

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Share this article directly by email. Simply enter the recipient’s details below.

Article has been send to you.